QDRO for Support

QDRO Past Due Child Support & Maintenance Arrearage

Most employer-sponsored retirement plans, including many pensions and 401(k) plans, are protected from ordinary creditor claims under the Employee Retirement Income Security Act of 1974 (ERISA). One important exception arises in the domestic-relations context, where retirement benefits may be assigned pursuant to a Qualified Domestic Relations Order (QDRO).

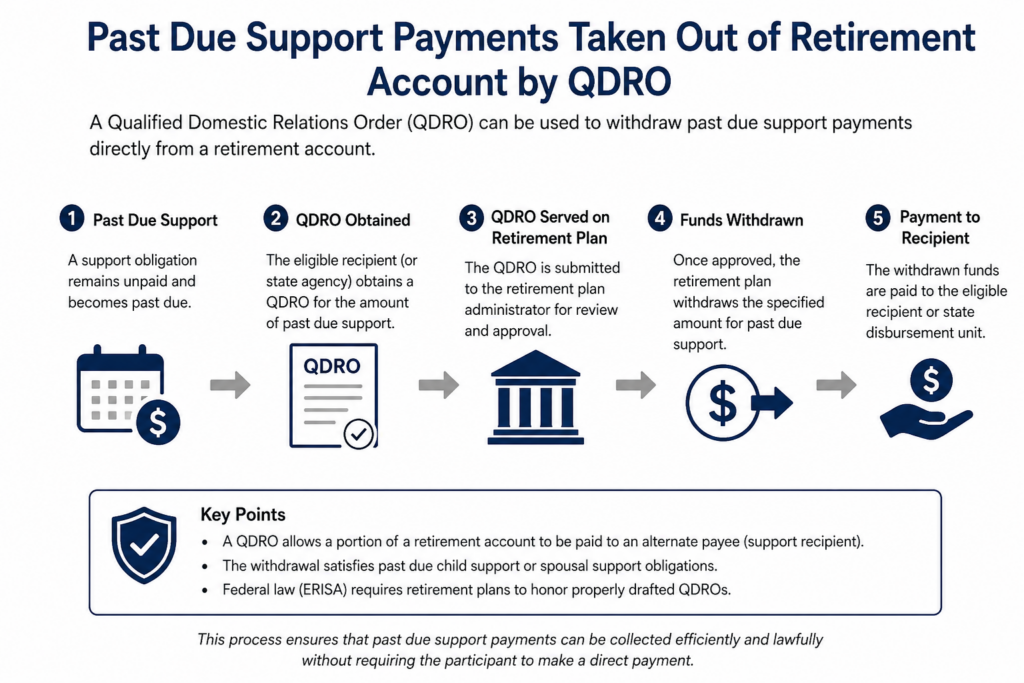

A QDRO is most commonly used to divide retirement benefits as part of the division of marital property. However, a QDRO may also be used to provide for the payment of child support or maintenance obligations.

For example, if a party owes past-due child support and wishes to resolve the arrearage through a lump-sum payment, but does not have sufficient non-retirement assets available, it may be possible to request entry of a domestic relations order assigning benefits from that party’s 401(k) plan, provided the order satisfies applicable statutory and plan requirements.

Similarly, if a party is owed child support or maintenance and the obligor lacks sufficient current income or other available assets, retirement-plan benefits may, in appropriate circumstances, be reached through a QDRO or comparable domestic-relations order, depending on the type of plan involved and the plan’s governing rules.

To qualify, the order must state the basis for the award and comply with ERISA, the Internal Revenue Code, and the plan administrator’s procedures. As a practical matter, it is often advisable to submit a draft to the plan administrator for review before seeking court entry.

Once the order is entered and determined by the plan administrator to be a valid QDRO, the administrator will implement the assignment and advise the alternate payee regarding available distribution or rollover options. In some cases, a distribution made pursuant to a QDRO may avoid the 10% early-distribution penalty, although income-tax consequences still must be considered.

If the retirement transfer is intended to resolve a support arrearage or other settlement obligation, it is often advisable to enter a separate agreed order setting out the terms of the parties’ settlement in addition to the QDRO itself.

Because retirement plans vary, the required procedure depends on the type of account involved; some plans are governed by ERISA and require a QDRO, while others are not.

The above is general guidance, not actionable legal advice. Please speak with an attorney.